Share on Social 👇

Taxability Of Capital Assets In India – All You Need To Know

The Capital Assets are specifically defined under Section 2(14) of the Income Tax Act specially defines capital assets. As per this definition, it means

- Property of any kind held by an assessee

- Securities recognized by SEBI, held be a Foreign Institutional Investor

- ULIPs to which exemption under Section 10(10D) does not apply

- Urban agricultural land

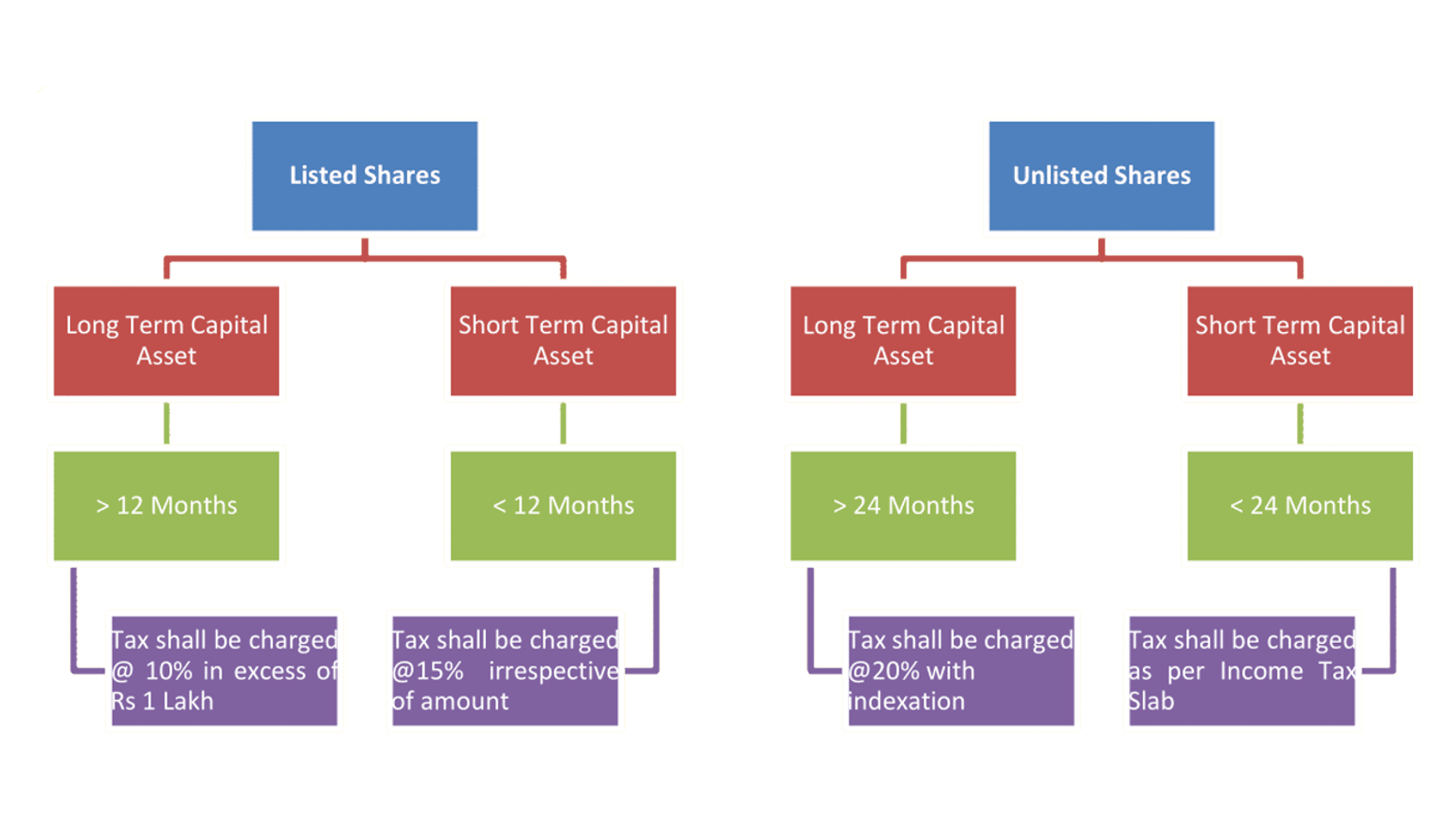

Shares

If the assessee holds the shares for trading purposes, then it is not treated as a capital asset. However, if he holds these shares for non-trading purposes, then it is treated as a capital asset. Further, the stocks are divided into two parts:

- Listed Shares

- Unlisted Shares

The taxability on the sale of shares on the basis of type and duration are as follows:

Mutual Funds

Mutual funds being movable property are capital assets. The mutual funds are of types:

- Equity Oriented Mutual Funds (investment in equities is more than 65% of the total portfolio)

- Debt Oriented Mutual Funds (investment in equities is less than 65% of the total portfolio)

The taxability of these types of mutual funds and is dependent on the duration of holding. Moreover, it is as follows:

| Funds | w.e.f 11 Jul, 2014 | On or before 10 Jul, 2014 | ||

| Long Term Capital Gains | Short Term Capital Gains | Long Term Capital Gains | Short Term Capital Gains | |

| Equity oriented Funds | Tax shall be charged @10% in excess of Rs 1 Lakh | Tax shall be charged @15% irrespective of amount | NIL | Tax shall be charged @15% irrespective of amount |

| Debt Oriented Funds | Tax shall be charged @20% with indexation | Tax shall be charged as per Income Tax slab | 10% without indexation or 20% with indexation whichever is lower | Tax shall be charged as per the Income Tax Slab |

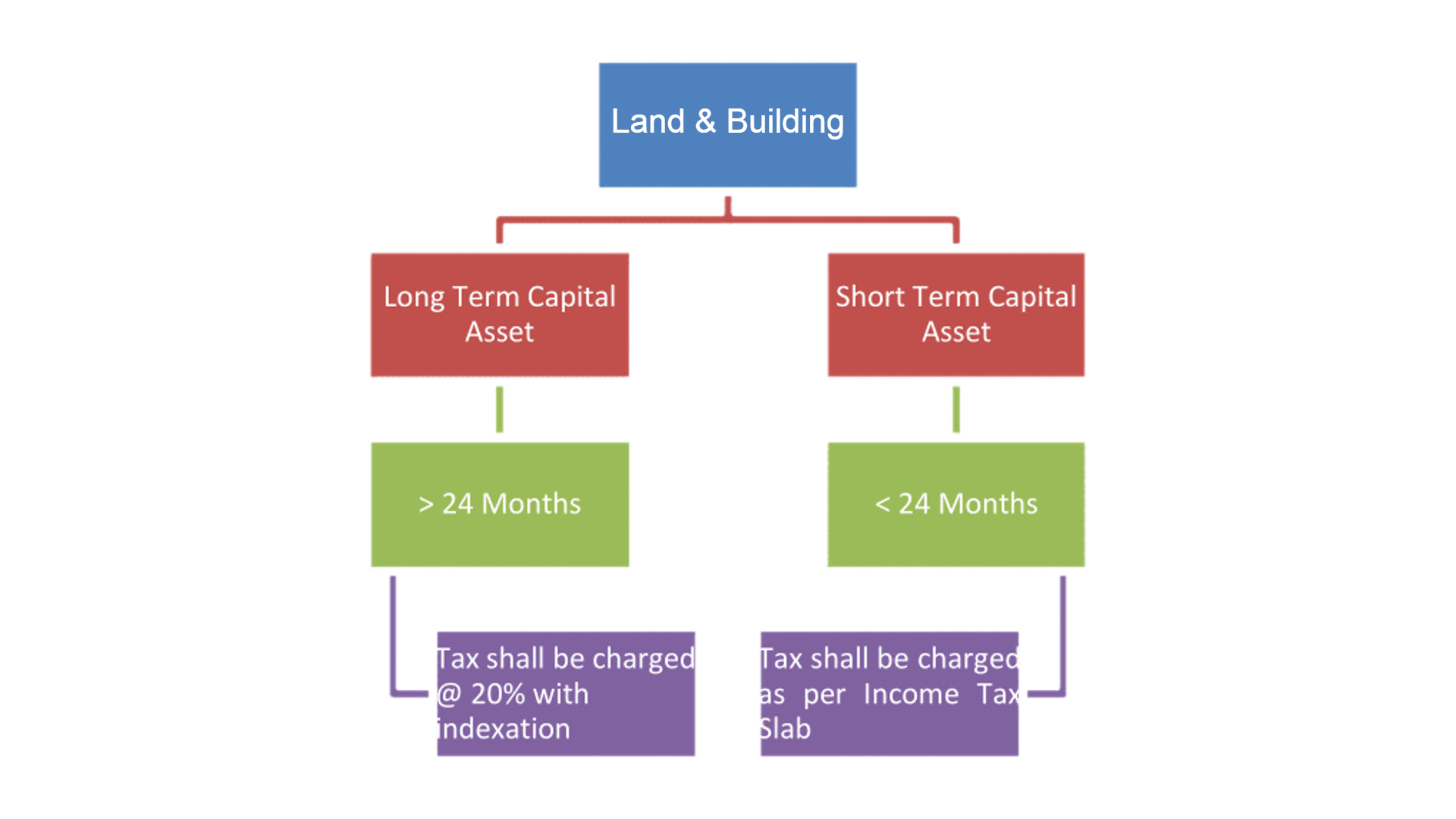

Land & Building

Land & building is a property which is also a capital asset and the profit on sale of such land and building is a capital gain. Moreover, the taxability rates on the basis of duration are as follows:

Cars

Car is a capital asset if it is used for business purposes because it allows in the purpose of depreciation. On the other hand, car purchased for personal purposes is not considered to be a capital asset.

Jewellery

Jewellery like gold, silver, diamond, precious stones, etc. are also capital assets. Consequently, any profit made on sale of it is treated as capital gain.

{kind=link}

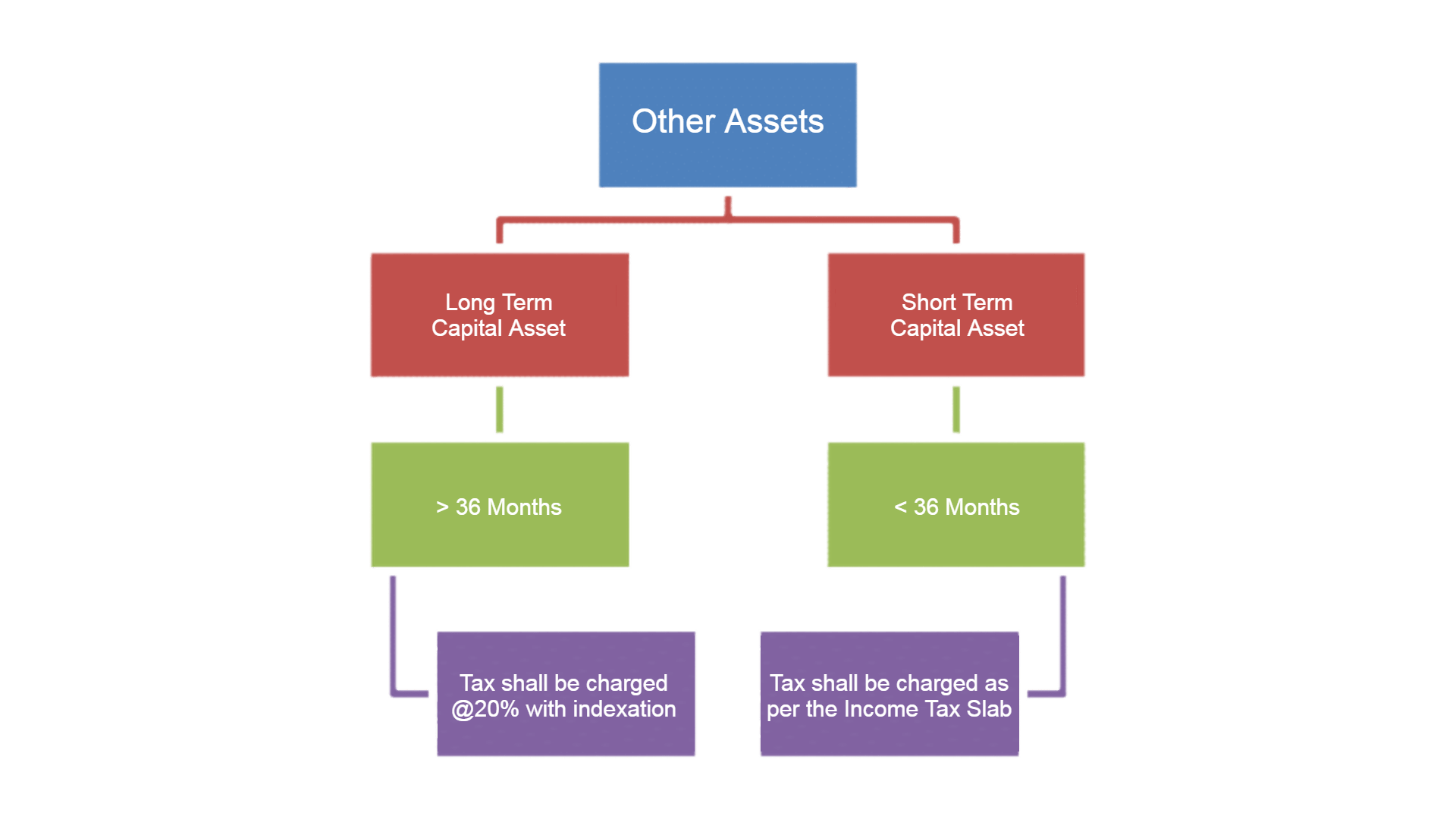

Some Other Examples Of Capital Assets:

Consult a C.A

Got a query? Talk to a Chartered Accountant. Click on the button 👉