ITC on Motor Vehicle – All You Need To Know

ITC on motor vehicle is available on GST paid under certain circumstances. In this article, we’ve discussed everything about ITC on vehicle.

ITC on motor vehicle is available on GST paid under certain circumstances. In this article, we’ve discussed everything about ITC on vehicle.

The ITC on motor vehicle under GST is available if such motor vehicles are used for making the following taxable supplies. However, there are certain conditions:

- Input Tax Credit (ITC) is admissible for motor vehicles which are used or intended to be used for transportation of goods

- ITC shall be allowable for passenger transport vehicles which are having approved seating capacity of more than 13 persons (including driver). There is no such restriction on ITC in this respect.

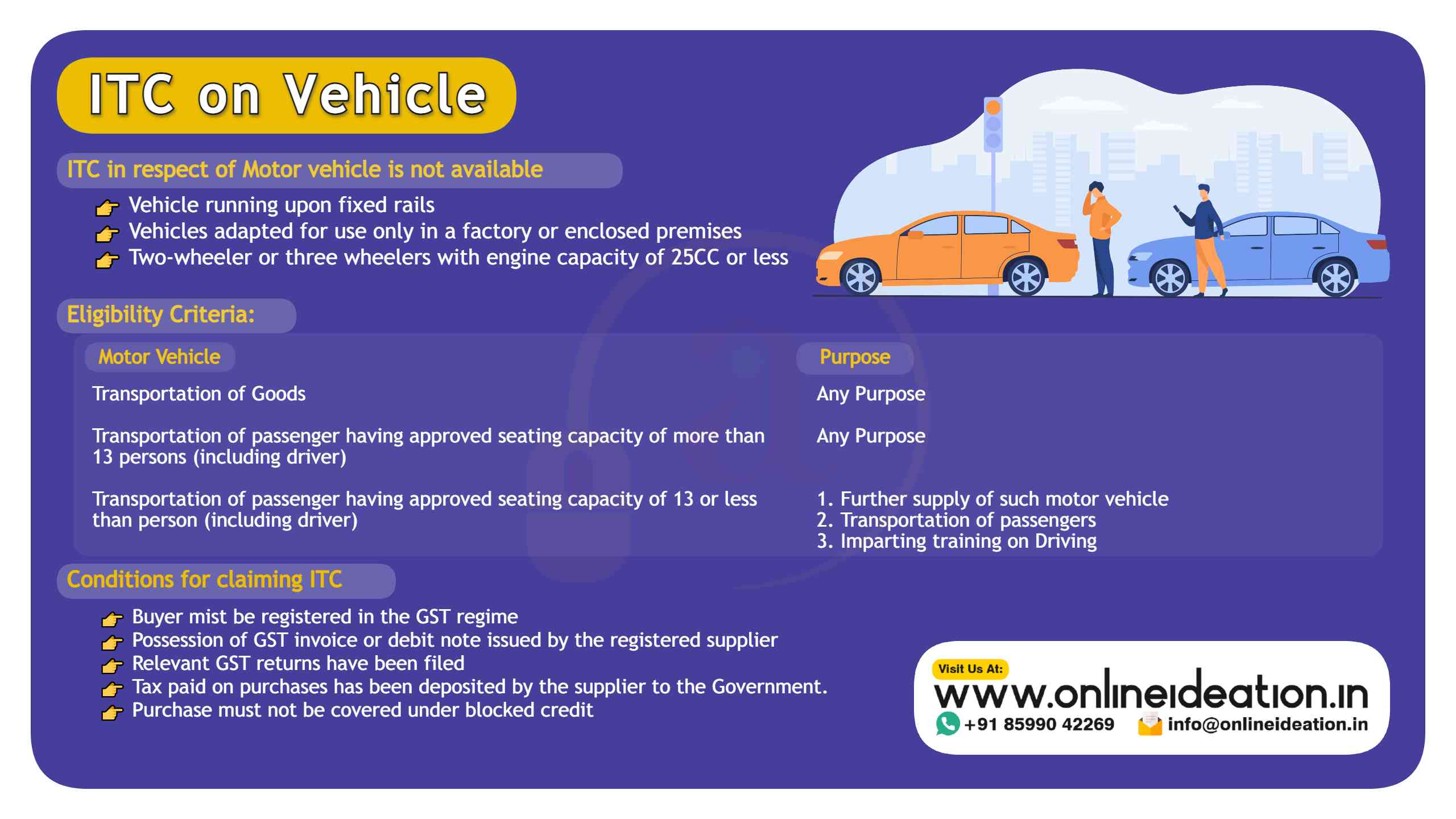

ITC in respect of Motor vehicle is not available

- Vehicle running upon fixed rails

- Vehicles adapted for use only in a factory or enclosed premises

- Two-wheeler or three wheelers with engine capacity of 25CC or less

Eligibility Criteria:

| Motor Vehicle Type | Purpose |

| Transportation of Goods | Any Purpose |

| Transportation of passenger having approved seating capacity of more than 13 persons (including driver) | Any Purpose |

| Transportation of passenger having approved seating capacity of 13 or less than person (including driver) |

|

👉 Read More: GST on Land & Building

Conditions for Claiming ITC

- Buyer mist be registered in the GST regime

- Possession of GST invoice or debit note issued by the registered supplier

- Relevant GST returns have been filed

- Tax paid on purchases has been deposited by the supplier to the Government.

- Purchase must not be covered under blocked credit

👉 Read About: GST ITC On Bank Charges – Everything to Know About

Cases Where ITC on Motor Vehicle Is Not Available

Read About: GST Rates On Textile And Garments

Read About:

Read About: Exceptions To ITC on Motor Vehicle Conditions