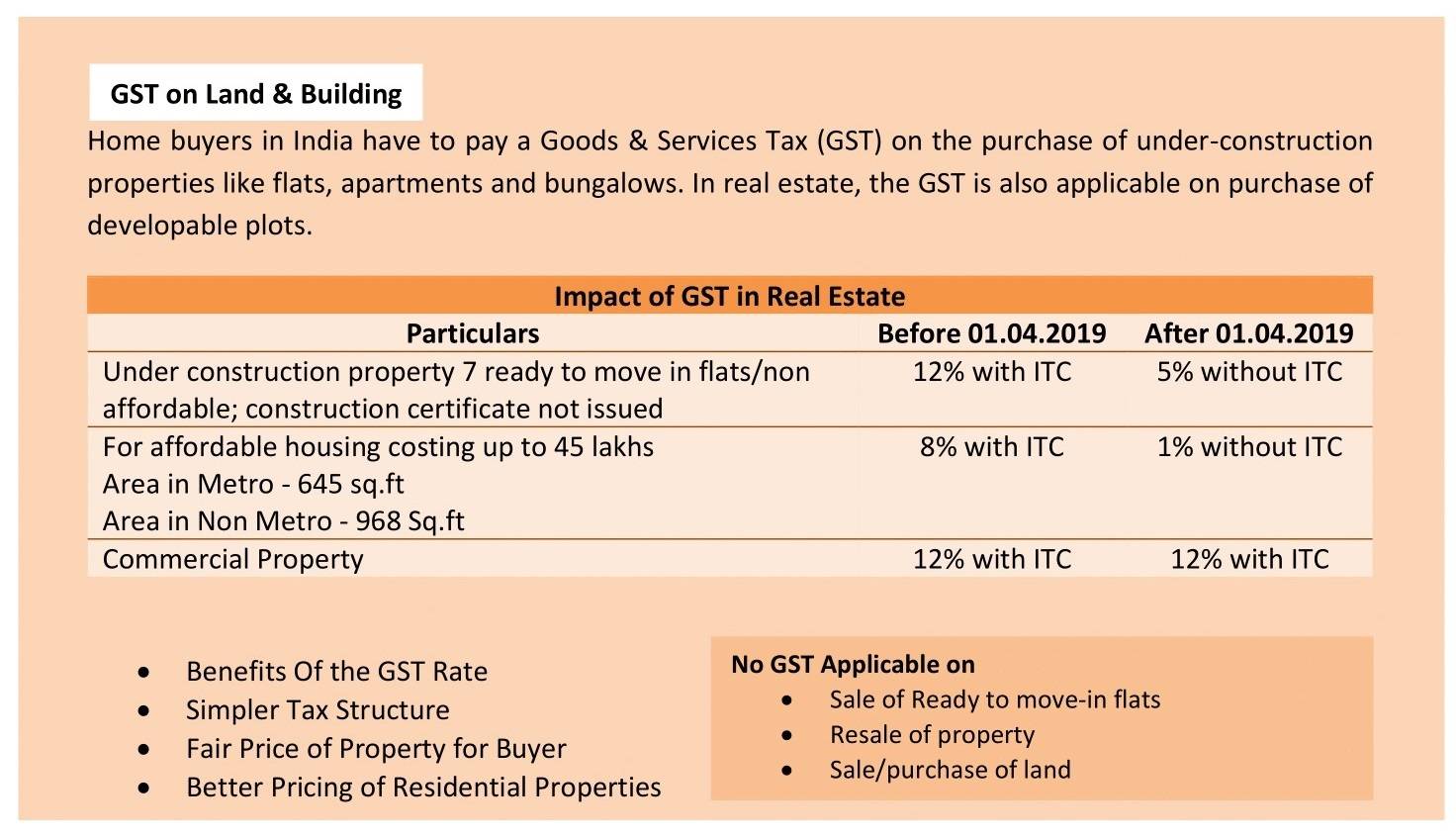

GST on Land & Building

GST regime considers selling of immovable property as supply of services. Therefore, GST is payable on the same. In this article, we shall talk in detail about GST on land and building.

As per Para 2 of the Press Release dated 19th March 2019, ‘ongoing projects’ has been defined as:

“a. Building where ‘construction’ started before 01.04.2019 and b. Building where actual ‘booking’ started before 01.04.2019 and c. Building which have not been completed by 31.03.2019”

Example:

Case | Construction before 01.04.2019 | Booking before 01.04.2019 | Completion by 31.03.2019 | Option to avail old rates? |

I | Yes | Yes | No | Yes |

II | No | Yes | No | No |

III | Yes | No | No | No |

IV | Yes | Yes | Yes | No |

There is no GST applicable on home loan repayment. However, the financial institutions providing the services of home loan, levy GST on processing fee, technical valuation fee and legal fee.

For GST Service (GST Registration & Return Filing, Click Here:

Book Service

Book Service

Book Service

Book Service